Consolidation and Timing

When an acquirer buys “control” of a target company, it will consolidate the results of the purchased company.

- The test for control is based on the ability of the buyer to dictate business decisions, which may be different than owning the majority of the shares of the acquired company.

- Consolidation means that the buyer will include 100% of the results of the target in its financials, and account for any remaining minority stake as noncontrolling interest.

The buyer will only begin to include the results of the target on the date the acquisition closes.

- This may mean the acquirer’s financials will contain a partial period of the target’s results unless the deal closed on the date of a period end.

Many merger models include a hypothetical “pro forma” combination analysis to show what the financials would have looked like if the deal closed at the beginning of a historical period.

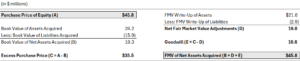

Purchase Price Allocation

When a company buys the equity of another company, the buyer uses its cash or issues new securities (debt or equity) to fund the purchase.

The buyer’s accountants will do an analysis to “allocate” the amount paid for the equity against the value of the assets, net of liabilities, acquired from the target. This ensures the buyer’s balance sheet balances after the deal by matching the amount spent in the deal to the value of the net assets acquired.

The attribution process is called Purchase Price Allocation (“PPA”) and is done to “explain” any premium paid over the book value of the net assets / equity (sometimes referred to as Excess Purchase Price).

PPA uses the Fair Market Value (“FMV”) of the target’s net assets as opposed to the historical carrying values (i.e. book value).

- Assets on a company’s balance sheet are often carried at historical cost and some assets don’t actually appear on the balance sheet under normal circumstances (i.e. brands).

As part of PPA, the assets and liabilities will be marked to fair value to help explain the gap between purchase price and book value.

- These FMV adjustments might be on tangible assets (i.e. machinery) as well as on previously unrecognized intangible assets such as customer lists and brands.

Any unexplained difference between the equity purchase price and the FMV of the acquired net assets (excluding pre-existing target Goodwill) is then allocated to an indefinite life intangible asset called Goodwill, or the “unexplained” portion of the Excess Purchase Price.

EXAMPLE:

Goodwill is therefore what ensures the buyer’s balance sheet balances. From the buyer’s perspective, it might present the value of some of the synergies it paid for and hopes to realize.

Tax Considerations

When the buyer purchases the shares of the target to get control of the business, as opposed to buying the actual assets, this triggers a tax consideration to be mindful of in merger modeling.

As part of the PPA process, if there are accounting FMV write-ups on assets that have a finite life, those assets will need to be amortized going forward.

But because the write-ups affect the accounting carrying value of the assets, but not the tax carrying value of the assets, this will create a mismatch between accounting pre-tax income and government pre-tax income over the life of the written-up assets. The company won’t be able to deduct the incremental amortization for tax purposes.

As a result of the added accounting amortization expense with no corresponding tax deduction:

Accounting Pre-tax Income < Government Pre-tax Income

Accounting Tax Expense < Taxes Payable to Government

Retained Earnings Decline < Cash Decline

To reconcile this mismatch over time, a Deferred Tax Liability (“DTL”) is created on the acquirer’s balance sheet at closing.

The new DTL is reduced each year (by recognizing a deferred tax benefit on the income statement) over the written-up asset’s life.

This ensures the balance sheet continues to balance since cash declines more than retained earnings:

Retained Earnings Decline + DTL Decline = Cash Decline from Taxes Payable

![]()

Even if newly recognized assets do not have a useful life (i.e. indefinite life intangibles), a related DTL is still recognized at closing due to the mismatch in the carrying value. If the asset is sold in the future, the accounting gain / loss will differ from the government gain / loss and the DTL will be reversed to reconcile the accounting vs. cash impact.

Impact on Forecasting

Since the PPA process will typically result in newly created assets on the buyer’s balance and associated amortization, this will reduce the combined company’s Net Earnings in the future.

- Neither company would have recognized these new assets if it weren’t for the acquisition.

Merger models will need to include the impact of these write-ups and tax implications on the buyer’s forecasted financials.

Sometimes models will show the impact on the buyer’s income both before and after the impact of the incremental amortization since the amortization is a non-cash expense.